“Cash or credit?” “Arch, btw.”

I wonder what distro they use

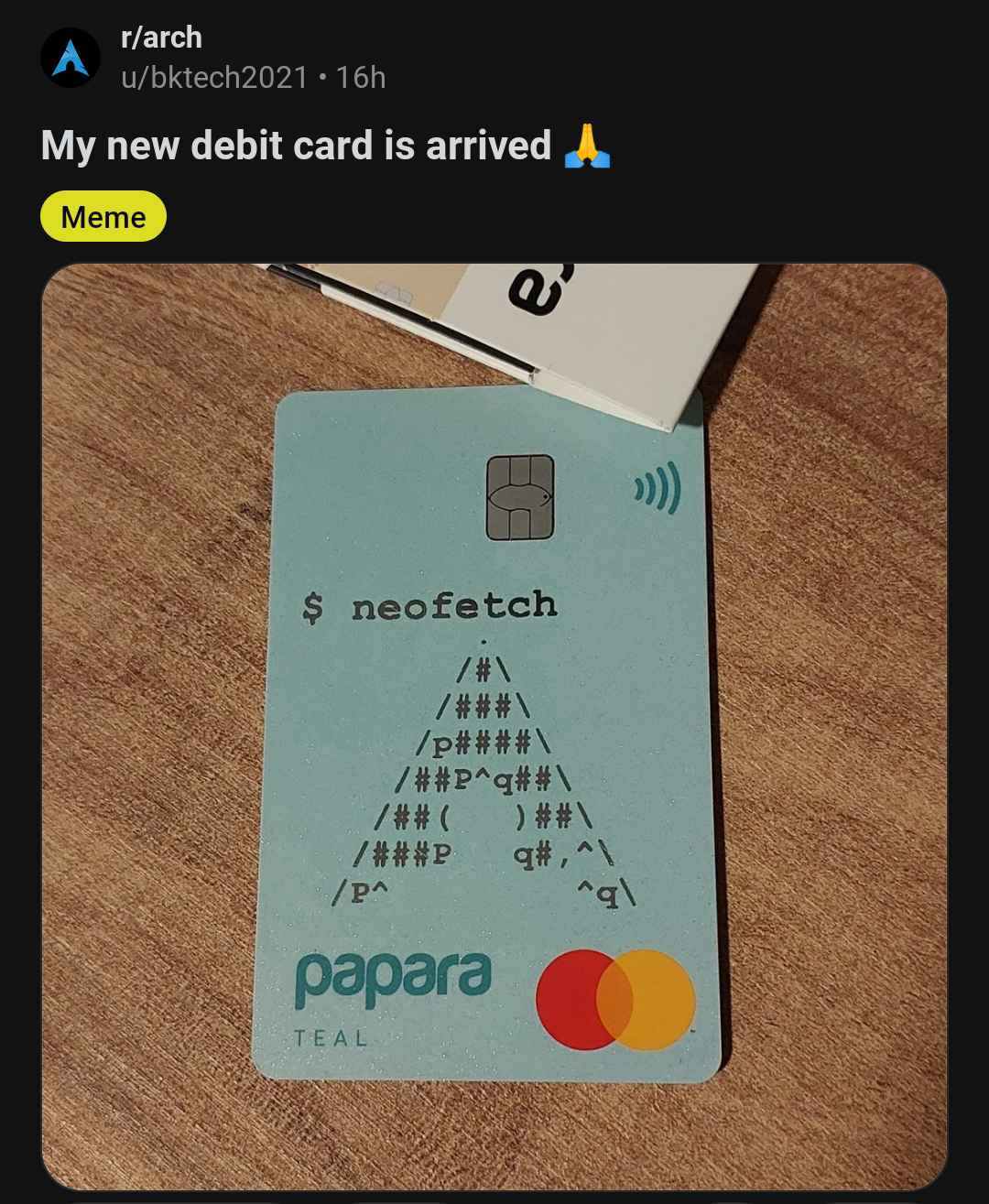

This is what happens when you think manually partitioning disks and chrooting makes you leet.

When I made a new linux install I chose Arch. I think for me the reasoning is thus. While I have a LOT of experience with unborking server linux installs, with desktop it’s just a pain to deal with. I previously used Manjaro which, while very easy to install, does obfuscate a lot of what happens behind the scenes. When it goes wrong, personally I found it harder to fix.

With Arch, beyond enough to give me a terminal and basic gnu tools, I’ve chosen what I install from then on. I think that means when things go wrong there’s a much higher chance I’ll know what it is and how to solve it.

Time will tell if this plan works out or not though :P

I’ve had the same path as you. Arch has been the simplest distro I’ve tried. And with archinstall it’s a breeze.

I’ve also found that Plasma 6 takes away most of the hassle with setting up a desktop - for my use case.

Been using a PC since Win 3.1 and it’s by far the most stable system I’ve ever had

show the back

As entertaining as that is, it does raise the question - why do they put all of the details on the back now?

I thought one of the main reasons that the CVV was on the signature strip was so if a card was photocopied, photographed, or carbon copied (literally on carbon paper), then it was still less possible to clone the card.

Is “physical” cloning so small of a problem now that it’s more beneficial to make fancy looking cards? Anyone in the industry able to shine a light?

This is an EMVCo chip card, and not an American one so it’s chip and pin most likely. Without getting too detailed, the chip generates a one time use code for each transaction, so just having the number wouldn’t help with cloning the card plus you also would need to know the PIN. Although skimmers still exist and physical card theft is a thing, it’s less common especially in markets that use chip and pin.

Absolutely spot on, thank you - always handy to know.

I’m wondering what it does to mitigate the “card not present” fraud though, for online purchases or remote purchases?

I’m in the US, and all of my cards have the numbers on the back now, and they’re not raised. I’m pretty sure we transitioned to chip and pin like a decade ago.

Furthermore even if a card is skimmed these days, at least in the UK, it’s still unlikely transactions would be processed online.

That’s because it’s become so commonplace now for transactions to pop-up in the banks app on the owners phone and they must confirm the transaction and / or receive a code via SMS. Some just use SMS as a means to confirm a transaction.

I guess one vector for attack still remains and that is SIM swapping, but even that is more difficult these days due to widespread awareness from carriers.

It depends. I got a new MasterCard debit card last week, and the numbers are on the front. Only the CVV is on the back.

Never leave the home directory without it!

{kind=link}

{kind=link}