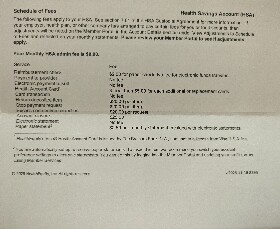

That schedule of fees looks like it’s straight from the 1980’s.

It deceives people whose idea of how things work in large companies hasn’t changed since the days when it was the manager of your bank branch who decided if you you should get a loan or not.

Nowadays, for certain in middle and large size companies, all the administrative main business pathways are heavilly if not totally automated and it’s customer support that ends up eating the most manpower (which is why there has been so much of a push for automated phone and chat support systems, of late using AI).

Those $25 bucks for “account closure” pays at worst for a few minutes of somebody’s seeking the account from user information on a computer, cross checking that the user information matches and then clicking a button that says “Close accout” and then “Ok” on the confirmation box and the remaining 99% or so left after paying for that cost are pure profit.

This is because you are not the customer. Your employer is the customer, they are the ones who get to choose the HSA provider for their employees. You are the goods to be sold. The HSA provider is simply harvesting profits.

“You are not the customer, you are the product” is true so often, but in many cases (like this one) it doesn’t really apply.

First off, “not the customer but the product” is an inherently antagonistic relationship. Your goals are opposed to Facebook’s, for instance, because you want to spend less time on the platform and you want to interact with friends and not brands, but Facebook wants the opposite of both. But with HSA administration, your goals and your employer’s goals are aligned: you both want someone who will quickly and painlessly manage your account without being a pain.

Second, “not the customer but the product” implies an undisclosed, extractive payment occurring behind the scenes. TikTok is harvesting a great deal of data from you and selling it to other companies. You are the product in that your data has value. But with HSA administration, the product is just the management of your HSA money; there’s no under-the-table dealing going on here (or there shouldn’t be); they’re getting paid by your company for their services.

Third, “not the customer but the product” relationships are entirely one-way; you have no way to impact the providing company beyond just not using their services. They do not, will not, and at some level can never care about your experience beyond making it as minimally useful to you to keep you on the platform. But that HSA provider desperately needs your company’s business, so if enough of your coworkers raise a stink and get your company to complain, they will make a change.

In actuality, “not the customer but the product” ignores the unfortunate reality of most HR/payroll service companies in this case: they’re just the lowest bidder, contracted at the bottom dollar to provide the cheapest services possible, because your employers don’t have to use their services and don’t care about your experience.

CFPB is aware of the issue. I’m guessing that the incoming administration is not going to care about fees.

And thank GOD! if a Business wants to Steal ALL my Money that just makes them GOOD BUSINESSMEN! If I wanted Rights I would Lift up my Bootstraps!

When I was looking for a non-employer HSA, there’s a lot of providers out there with not-exactly-predatory terms. All kind of fees or restrictions that you wouldn’t find on other types of checking/saving/brokerage accounts. I ended up a Lively, but they added some investment/transfer fees when Schwab bought Lively’s investment partner TDA.

I suspect it’s partly because most HSA are determined by the employer, so someone in HR can be induced to choose a fee-laden plan if it’s easier for them, and partly because the tax benefits are so great that it still makes sense even after paying a $20 junk fee here and there.

Reminds me of when my ISP who was “no contract” had a cancellation fee. Like I have to pay money to stop being billed? Something about that feels very backwards.

{kind=link}

{kind=link}