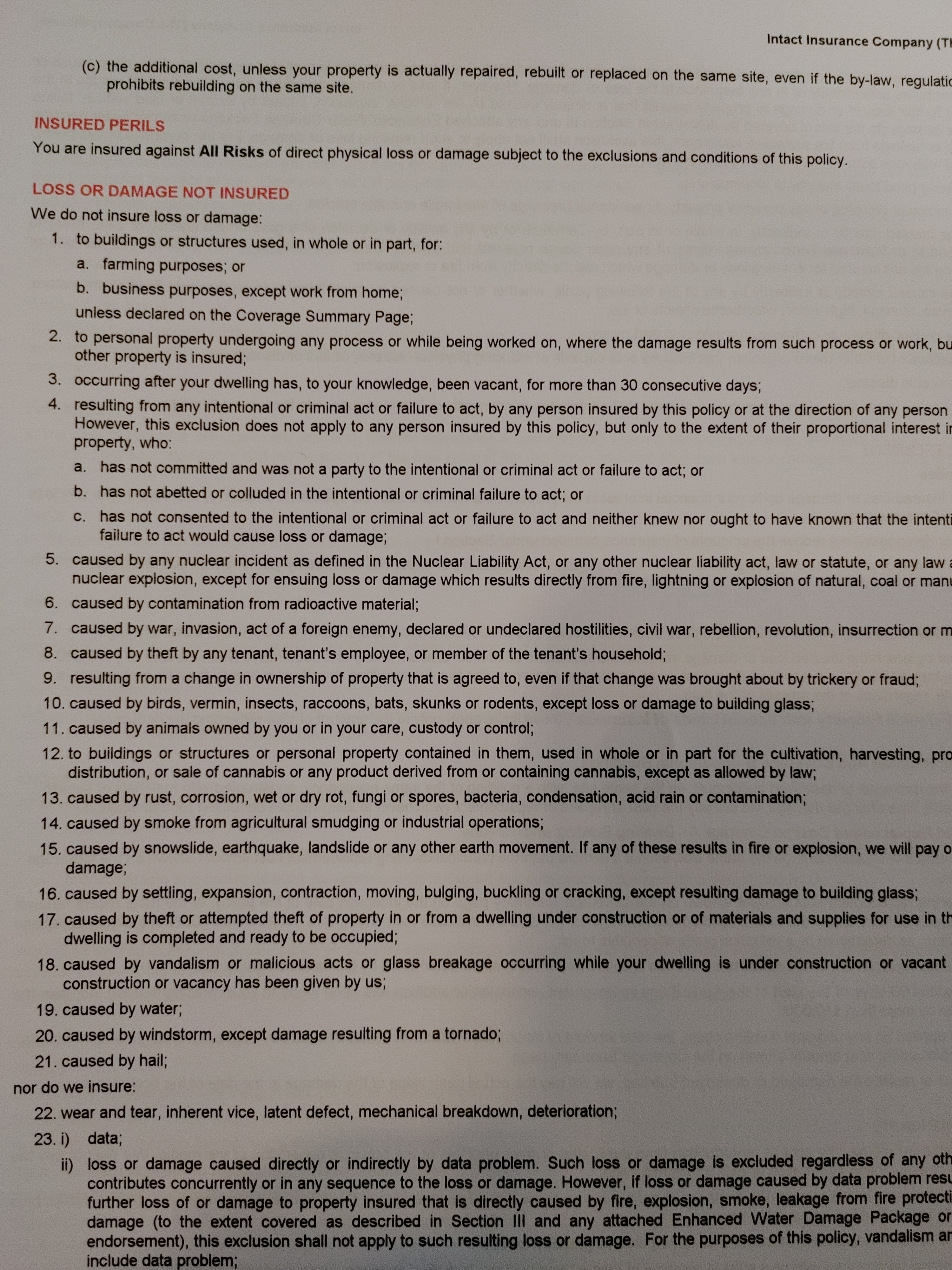

I was once given complimentary wheel and tire insurance which didn’t cover against accidental damage, wear and tear, road debris or malicious damage by another person. The only thing I could think it covered is if I slashed my own tires and also could prove it was me doing it

i like how nukes and war is 5-7 and then alllllll the way down they’re like, “oh also no water damage and no normal wear and tear.”

So basically they only insure against a stranger damaging it, and fire.

Hrm, this list seems a lot shorter than the one in the OP. It’d sure be nicer if they had just said your version…

It’s a contract. You can be sure they’re going to list just about everything.

Fuck homeowners insurance. I live in Florida. I’ve had State Farm for several years now, and it always felt like I was paying them extortion payments. Last year, we got a letter from them informing us that they had sent an inspector by our property, and listed off several things that we needed to do, and show them proof that we did them, within the next year or they were dropping our coverage. Some of these things were understandable, but others just seemed ridiculous. Like re-roofing or tearing down my shop in the back, when there is absolutely nothing wrong with it (I just built it seven years ago). It’s already pretty well-known that SF is no longer writing new policies in Florida, so I could see the writing on the wall. Even if we complied and got all that done, their premiums were going to go way up, and switching to another company would certainly cost us even more. The wife and I discussed it and said fuck it and fuck them and took the money out of my 401k and paid the place off. State Farm will not renew us here in about a month and a half when it expires, and we’ll carry on without. This house has been through every hurricane that’s hit the NW corner of Florida since 1958 and has so-far only lost some shingles. We’re on high enough ground that flooding isn’t a worry either, so fuck it… off we go, fingers crossed! I feel really fortunate that we were able to do that, because this place is so much more than just a house, and I’ll be DAMNED if we’re losing it because some bureaucratic requirement that I can no longer afford allows it to be repossessed.

Do they actually cover anything? For that “coverage”, they should pay you instead.

{kind=link}

{kind=link}